Planning for retirement is one of the most important financial decisions a person will ever make. Yet, for many people, retirement planning feels confusing, overwhelming, or easy to postpone. With so many retirement plans available—each with different rules, benefits, risks, and tax implications—it can be difficult to know which option is truly the best.

The truth is that there is no single “best” retirement plan for everyone. The best plan depends on individual circumstances, including income level, employment status, risk tolerance, lifestyle goals, and time horizon. Choosing the right retirement plan requires understanding how different options work and how they align with long-term financial objectives.

This article provides a comprehensive guide on how to find the best retirement plans. It explains key concepts, common plan types, evaluation criteria, and practical steps to help individuals make informed, confident decisions about their retirement future.

Why Retirement Planning Matters More Than Ever

Retirement planning has become increasingly important due to economic and demographic changes.

Longer Life Expectancy

People are living longer than previous generations, which means retirement savings must last longer. Without proper planning, there is a risk of outliving one’s savings.

Shifting Responsibility to Individuals

In many countries, responsibility for retirement income has shifted from employers and governments to individuals. This makes personal retirement planning essential rather than optional.

Inflation and Rising Living Costs

Inflation erodes purchasing power over time. A retirement plan must not only preserve savings but also help them grow to maintain a reasonable standard of living.

Understanding What a Retirement Plan Really Is

A retirement plan is a structured way to save and invest money specifically for use during retirement.

Core Purpose of a Retirement Plan

The primary goals of a retirement plan are to:

- Accumulate savings over time

- Generate income after retirement

- Provide financial security and independence

A good plan balances growth, stability, and accessibility.

Step 1: Define Your Retirement Goals Clearly

Finding the best retirement plan starts with understanding your own goals.

When Do You Want to Retire?

Your expected retirement age determines how long your money has to grow. A longer time horizon generally allows for higher-risk, higher-growth investments.

What Kind of Lifestyle Do You Want?

Consider:

- Housing costs

- Travel plans

- Healthcare expenses

- Daily living expenses

Your desired lifestyle directly affects how much you need to save.

Estimating Retirement Income Needs

While estimates vary, many planners suggest aiming to replace a significant portion of pre-retirement income. However, personal circumstances matter more than general rules.

Step 2: Understand the Main Types of Retirement Plans

Different retirement plans serve different needs.

Employer-Sponsored Retirement Plans

Employer-sponsored plans are often the foundation of retirement savings.

Defined Contribution Plans

These plans allow individuals to contribute a portion of their income, often with employer contributions.

Key features

- Contributions are invested

- Retirement income depends on investment performance

- Individual bears investment risk

Employer matching contributions can significantly enhance long-term savings.

Individual Retirement Plans

Individual plans allow people to save independently of their employer.

Key features

- Flexible contribution options

- Broad investment choices

- Personal control over strategy

These plans are particularly important for self-employed individuals or those without employer-sponsored options.

Government-Supported Retirement Programs

Many countries provide public pension systems funded through taxes or contributions.

Key features

- Provide baseline retirement income

- Not usually sufficient alone

- Often depend on years worked and contributions

Understanding how public benefits fit into your overall plan is essential.

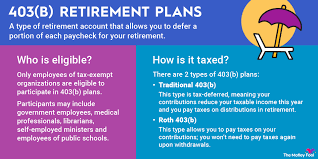

Step 3: Evaluate Tax Advantages Carefully

Tax treatment is one of the most important factors in retirement planning.

Tax-Deferred vs Tax-Free Growth

Some retirement plans allow investments to grow without being taxed until withdrawal, while others offer tax-free withdrawals later.

Choosing the Right Tax Strategy

The best option depends on:

- Current income level

- Expected income in retirement

- Future tax rate uncertainty

Tax efficiency can significantly affect long-term outcomes.

Step 4: Assess Investment Options Within Retirement Plans

Not all retirement plans offer the same investment choices.

Range of Available Investments

Plans may include:

- Stocks and equity funds

- Bonds and fixed-income investments

- Balanced or target-date funds

Greater flexibility allows more customised strategies.

Risk and Time Horizon

Younger individuals may tolerate more volatility, while those closer to retirement often prioritise stability and income.

Step 5: Understand Fees and Costs

Small fees can have a large impact over time.

Common Retirement Plan Fees

These may include:

- Management fees

- Administrative fees

- Fund expense ratios

High fees reduce net returns, especially over long periods.

Comparing Cost Efficiency

When evaluating plans, consider both:

- Absolute costs

- Value provided

Lower-cost plans often outperform higher-cost alternatives over time.

Step 6: Consider Contribution Limits and Flexibility

Contribution rules affect how much you can save.

Annual Contribution Limits

Many retirement plans impose limits on how much can be contributed each year. Higher limits provide greater savings potential.

Flexibility During Life Changes

Good retirement plans accommodate:

- Career changes

- Periods of lower income

- Self-employment

Flexibility supports long-term consistency.

Step 7: Evaluate Employer Contributions and Benefits

Employer contributions are effectively free money.

Matching Contributions

If an employer offers matching contributions, failing to participate fully can significantly reduce long-term savings.

Vesting Schedules

Understand how long you must remain employed to fully own employer contributions.

Step 8: Consider Portability and Accessibility

Life rarely follows a straight path.

Portability Between Jobs

A good retirement plan allows assets to be transferred easily when changing employers.

Access Rules and Penalties

Understand:

- Withdrawal restrictions

- Early withdrawal penalties

- Loan provisions

Retirement plans should discourage unnecessary withdrawals while allowing flexibility in genuine emergencies.

Step 9: Balance Growth and Security

Retirement planning involves managing trade-offs.

Growth-Oriented Strategies

Growth-focused plans aim to maximise long-term returns but involve greater volatility.

Income and Capital Preservation

As retirement approaches, shifting toward income and capital preservation reduces risk.

Step 10: Diversify Across Multiple Retirement Plans

Relying on a single plan increases risk.

Benefits of Diversification

Using multiple retirement plans can:

- Improve tax efficiency

- Increase flexibility

- Reduce reliance on one income source

Diversification enhances resilience.

Step 11: Adjust Retirement Plans Over Time

The best retirement plan today may not remain optimal forever.

Reviewing Plans Regularly

Life events such as marriage, children, career changes, or health issues require plan adjustments.

Rebalancing Investments

Periodic rebalancing ensures that risk levels remain aligned with goals.

Step 12: Avoid Common Retirement Planning Mistakes

Many people make preventable errors.

Common Mistakes

- Starting too late

- Saving inconsistently

- Ignoring inflation

- Taking excessive risk near retirement

- Failing to understand plan rules

Avoiding these mistakes significantly improves outcomes.

Step 13: Seek Professional Advice When Needed

Retirement planning can become complex.

When Professional Help Is Useful

Advice may be valuable when:

- Income is high or variable

- Tax situations are complex

- Retirement is approaching

Independent, fee-transparent advice is often most reliable.

Step 14: Build a Simple, Sustainable Retirement Strategy

Complexity does not guarantee better results.

Focus on Consistency

Regular contributions over time often matter more than perfect timing.

Align Plans with Personal Values

Retirement planning should support not only financial needs but also personal priorities and peace of mind.

The Role of Discipline and Patience

Retirement planning rewards long-term thinking.

Compounding Over Time

Starting early allows compound growth to work more effectively.

Staying the Course

Market volatility is inevitable. Staying committed to a well-designed plan improves long-term success.

Final Thoughts: Finding the Best Retirement Plans for Your Future

Finding the best retirement plan is not about chasing the latest trend or maximising short-term returns. It is about choosing a structure that aligns with your goals, risk tolerance, and life circumstances while providing tax efficiency, flexibility, and long-term growth.

The most effective retirement strategies:

- Start early and remain consistent

- Use tax advantages wisely

- Balance growth and security

- Adapt over time

- Focus on long-term sustainability

By taking a systematic, informed approach, individuals can transform retirement planning from a source of uncertainty into a source of confidence. The best retirement plan is not the most complex one—it is the one you understand, commit to, and maintain over time.

Summary:

How to Find the Best Retirement Plans

Keywords:

Retirement plan

Article Body:

You have been longing for the day that you no longer have to rush for the bus or step on that gas, head for the office as fast as you can in order not to be late.

All of these will come true by the time you reach your retirement age. It is a point in your life wherein work is no longer attractive yet income remains the top most necessity. If the day comes that you will no longer have to work, the biggest dilemma will be on what will happen next?

A retirement plan is a requirement if you are to take pleasure and benefit from the moment after you have decided to retire.

Most often than not, people are not concerned about retirement plans. They simply pass the time and believe that retirement will eventually take place, with or without retirement plan.

What they failed to realize is that creating a retirement plan is the next most important thing any working individual should work with. What lies ahead is never too clear for people who do not have solid retirement plans.

What Is Retirement Plan?

Retirement plans are, forms of agreement that cater to give people with a considerable amount of money by the time they have reached their retirement age. These amounts are enough to compensate their continuous struggle for existence even if they are no longer working or earning the kind of income they used to make before.

In most cases, retirement plans are established by government, employers, trade unions, or some financial institutions such as insurance companies.

In essence, there are only two major types of retirement plans � �defined contribution� and �defined benefit.� These plans are classified according to how the remunerations are resolved.

Defined contribution refers to retirement plans that will give disbursements based on the amount of contributions that the benefactor has paid.

On the other hand, defined benefit refers to a particular type of retirement plan wherein the disbursements are based on the flat rate as computed from the employee�s membership years and the amount of his income while employed.

Considering these facts, not all retirement plans are deemed equal. Hence, it is best to analyze your status and determine what type of retirement plan will work best for you. You need to consider some factors to help you with your decision.

- Reflect on the advantages and benefits

Retirement plans were especially designed to give you the benefits that you need by the time you reach your retirement age.

However, not all benefits are the same. What may seem beneficial for the others may not necessarily work for you.

Therefore, consider the type of benefits that you need and consider them upon evaluating a particular retirement plan.

- Know the law

Be sure that the retirement plan that you will take is inconformity with the present law on retirement. This will guarantee your safety in the future.

- Read the fine print

Reading the fine print is important in analyzing the reliability of a particular retirement plan. Every benefit and rule should be explained in details through the catalog.

If you think that the conditions are too good to be true, then, they probably are. Hence, try to consider other choices.

Familiarize yourself with retirement plans before making a decision. This will help you create a dependable future ahead.

Tinggalkan Balasan